Carnegie Endowment hosted a session about global recovery in the aftermath of the global financial crisis yesterday. Four analysts shared their forecasts and views about where the global economy is heading now.

Hans Timmer, lead economist of Development Prospects Group at the World Bank, argued that though gradual recovery is happening , the pace would depend not only on performance of the US economy but also on the magnitude of rebound in the emerging economies. During the crisis, the emerging economies plunged the most, so in order to rebound strongly, they have to grow strongly. He argued that Fareed Zakaria's misread the numbers in his recent column in the sense that he holds the view that if the US spends enough, things will be okay. Rebound in the developing countries, especially the emerging economies, will determine how fast the global economy will be pulled out of this mess. In the emerging economies, the decline in imports was higher than the decline in exports; the opposite is true for high-income countries. The developing countries reconsidered their investment projects and used up their inventories while reducing imports, deepening the crisis.

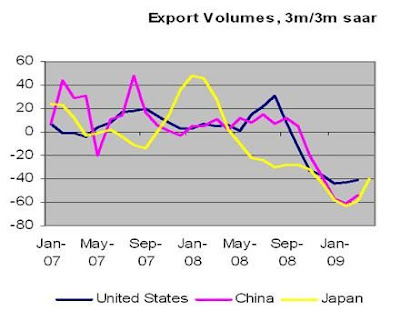

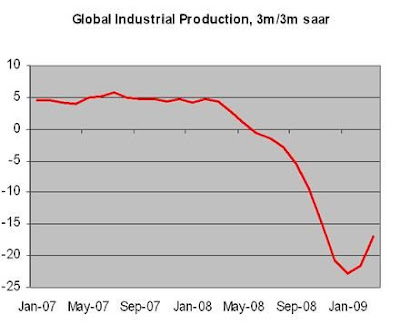

He opined that the present rebound (industrial production), which has been visible since the first quarter of 2009, does not reflect a real recovery and might just be a "technical rebound". In the last five months, Asian exports and imports have increased. Japan’s growth is driven by imports by other Asian nations. Commodity prices have also begun to move up. The strength and sustainability of rebound would depend on investment levels and inventories build up and the looseness of international credit supply.

Jorg Decressin, division chief of European Department at IMF, argued that the global recovery is definitely real but is heavily policy dependent. It is a subdued recovery. Consumer confidence is gradually rebounding and so is trade. Interest rate is near zero and a lot of liquidity has been injected into the global economy. However, for sustainable recovery, private demand has to take the place of public demand. Moreover, global imbalances in trade have to be corrected and fiscal deficits have to be brought down. External deficit countries will have to invest less and save more while external surplus countries have to invest more and save less. China alone cannot do it because Chinese total consumption is almost 25 percent of the total US consumption. The Middle East countries also have to step in but they too are constrained by their own challenges. So, rebalancing will take time and recovery will be slow. It is not a self-sustaining recovery.

Philip Suttle, director of Global Macroeconomic Analysis at IIF, argued that the rebound is real and does not look “technical” to him. He made six points:

- Inventories will be rebuilt steadily rather than suddenly in the coming quarters

- Global financial condition is getting better. The transmission mechanism of money is working pretty good

- There is an upward revision to capital spending plans

- Housing collapse appear to be ceasing, especially in the US and UK

- Fiscal stimulus is starting to kick in.

- Labor market conditions will begin to improve.

All these positive signs signal that rebound is real and the trend is upwards. However, there are chances of “double-dip”, as happened during the first half of 1980s, but is not very likely. Events that could cause “doubled-dip” are (but unlikely):

- Emerging markets don’t deliver

- More financial turmoil (like Lehman Brothers debacle)

- High inflation forcing policymakers to tighten up monetary and fiscal policies (he argues that this is possible because our errors in predicting inflation have typically been on the high side)

Uri Dadush, director of International Economics program at Carnegie, argued that stimulus and credit restoration has led to nascent recovery. Rebounding might be slow but it cannot be too slow because it is already a very low level. He argued that in six to twelve months from now, the stimulus will have to be withdrawn. The recovery will then depend on how much the private sector will be able to pick up from the public sector-driven growth path. In the next six months, recovery will persist. Asia, the Europe, and the US have to rely on their own restructuring and domestic demand for sustained growth, he said.

The discussion was focused exclusively on the emerging economies and the OECD countries, though the panelists kept on saying ‘developing countries’, trying to mean as if they were talking about the whole world. Nobody even mentioned Sub-Saharan Africa (except for Hans, who briefly said the focus of the next G20 would be on the developing countries, poverty reduction, and the financial crisis’s impact on the poor). No trading blocs like SAARC, SADC, AU, MENA, and BIMSTEC, among others were mentioned. It might partly be because only a handful of countries drive the global trade and economy and if they don’t grow, others might not as well.

Also, it appeared that the recovery they were talking about was based on the existing system. What would a recovery look like in a reformed system, where some banks are nationalized and investment banks and hedge funds are under tight supervision? The looseness in credit from these institutions is already restrained. Moreover, a huge chunk of liquidity and investment source-- derivatives markets-- is pretty much in doldrums now. So, the recovery now look like just stocking up of inventories. After it is near-full, the real recovery would actually depend on how we fill up the liquidity void created by busted investment banks, hedge funds, subprime markets and derivates markets. Due to these markets’ absorptive capacity, inflation was pretty low despite high liquidity in the past seven years (?!?). It won’t be the same now. So, where will the trend in recovery stop or satiate?