Nepal: Mid-year review of FY2017 budget and monetary policy

The Ministry of Finance released its mid-year review of FY2017 budget. It increased revenue target but lowered expenditure target. There is not much change in expenditure pattern. Actual capital spending was just 11.3% of planned capital spending. However, the government is targeting to bump this to 84% by the end of the fiscal year. Around 49% of total revenue target was achieved by mid-year.

The NRB also released its mid-year review of FY2017 monetary policy and macroeconomic situation. Inflation averaged 5.8% on the back low fuel and commodity prices, good monsoon-led boost in agricultural output, normalization of supplies and decreasing inflation in India. Current account slipped in the negative territory due to the widening of trade deficit and deceleration of remittance inflows.

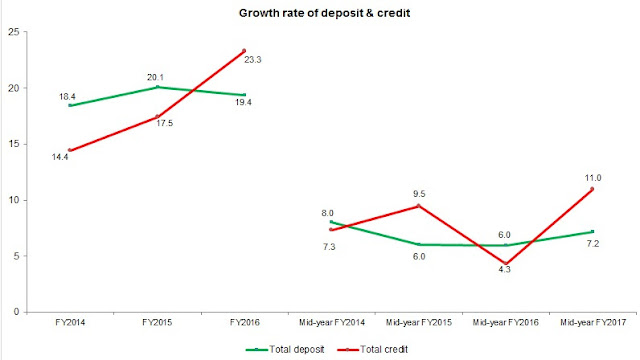

The NRB also tweaked accounting rules on computing CCD ratio. It has allowed BFIs to discount 50% of productive lending (plus lending to deprived sector and lending to agro sector at subsidized interest rate) while computing the CCD ratio. This essentially gives a breathing space to many BFIs that are close to the mandatory threshold of 80. It frees up about NRs130 billion for extra lending (by mid-year BFIs lent about NRs254 billion to productive sector).

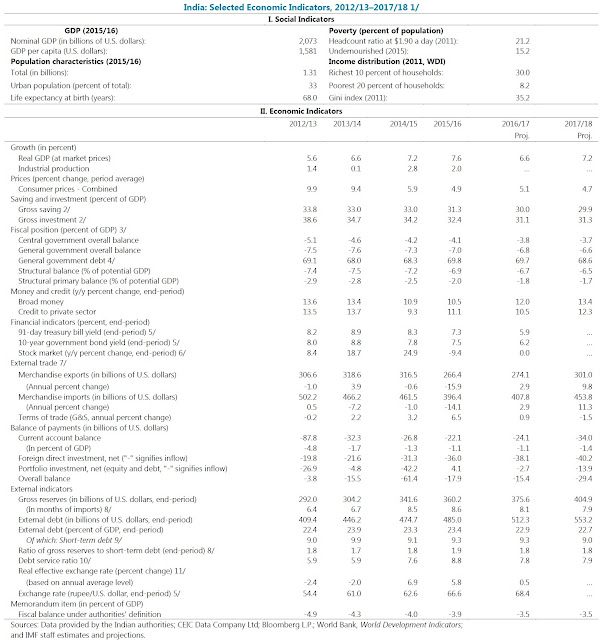

India: Macroeconomic overview (IMF)

- Real growth (at market prices) projected to slow to 6.6% in FY2016/17 and then rebound to 7.2% in FY2017/18

- Normal monsoon rainfall but suppressed private consumption demand (due to demonetization shock)

- Low inflation of around 4.7% (temporary demand disruptions due to demonetization, good agricultural harvest due to good monsoon, collapse of global commodity prices, supply-side measures, tight monetary policy stance)

- Reduced external vulnerabilities (CA deficit to remain low and international reserves to cover around 8 months of import), and large terms of trade gain (increased by 2.22% in

- FY2013/14, 2.5% in FY2014/15, and 7% in FY2015/16)

- Focus on fiscal consolidation and quality of public spending (FY2015/16 budget deficit of around 3.9% of GDP; FY2016/17 budget on track to reach 3.5% of GDP target)

- Implementation of key structural reforms including GST (has the potential to raise medium-term growth to above 8%), using Aadhaar identification and bank accounts to make direct benefit transfers, formalization of inflation targeting framework, new Bankruptcy Act

Key challenges: persistently high household inflation expectations, large fiscal deficits, excess capacity in key industrial sectors, strains in financial and corporate balance sheets, the extent of cash shortages, external vulnerabilities (global financial market volatility including from US monetary policy normalization and weaker-than-expected global growth).