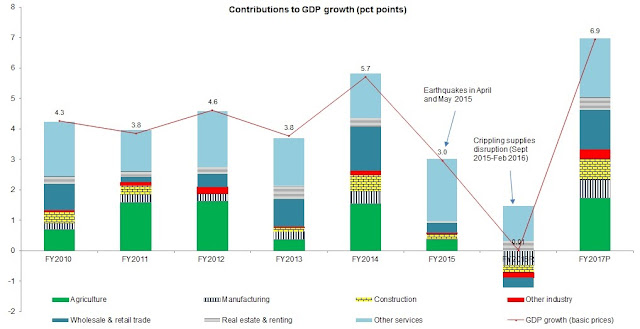

On 25 April, Central Bureau of Statistics (CBS) estimated that Nepal’s economy would likely grow by 6.9% in FY2017, sharply up from 0.01% in FY2016 and 3% in FY2015. This is the highest GDP growth rate (at basic prices, FY2001=100) since FY1994 (when GDP grew by 7.9%) and is higher than the government’s target of 6.5%. It projected agricultural, industrial and services will grow by 5.3%, 10.9% and 6.9%, respectively. Agricultural sector contributed 1.7 percentage points, industrial sector 1.6 percentage points and services sector 3.6 percentage points to the overall projected GDP growth of 6.9%. These projections are based on eight to nine months data.

Specifically, electricity, gas and water sub-sector will likely grow at fastest rate (a whopping 13%) compared to a negative 7.4% growth in FY2016. Similarly, construction activities will likely grow at 11.7%, up from a negative 4.4% in FY2016. Wholesale, and retail trade, and manufacturing are projected to grow by 9.8% and 9.7%, respectively (up from negative growth rates in FY2016).

An obvious query is: how is this possible? Well, it’s a combination of base effect, good monsoon, improved supply of electricity and normalization of supplies following the catastrophic earthquakes in FY2015 (April and May 2015) and the crippling supplies disruption in FY2016 (September 2015-February 2016). A growth rate of around 6% was expected.

First, it’s the base effect, which refers to the tendency of achieving an arithmetically high rate of growth when starting from a very low base. Hence, only the normalization of economic activities disrupted by the crippling embargo and the lingering impact of the earthquakes would have generated a high growth rate. Note that FY2017 is compared to the performance in FY2016, when growth was almost negligible (0.01%). Even a slight improvement in the normal drivers of growth would have produced a large growth rate in FY2017. Indeed, the seven highest growing sub-sectors in FY2017 had negative growth rates in FY2016 caused by the crippling supplies disruption, which dented economic activities much more than the earthquakes in FY2015. Similarly, agriculture and forestry subsector grew at a negative 0.2% in FY2016 due to the subnormal monsoon, and continued land and harvest disruption caused by natural disasters.

Second, an above average monsoon rains led to record paddy harvest and consequently an impressive agricultural growth. This is an exogenous positive shock. The government also adequately supplied agricultural inputs (including chemical fertilizers and seeds) and restored irrigation facilities (depreciation, and disruption by earthquakes and landslides). It also helped. Paddy output is projected to grow by 21.7% (paddy alone contributes 20.7% to agricultural gross value added). Wheat and maize outputs are projected to grow by 2% and 1.3%, respectively.

Third, the industrial sector pretty much got a facelift, thanks to the sound management and supply of electricity, improved investor confidence, and pick up in post-earthquake reconstruction works (both private and public). This is where the government’s efforts are most visible. The demand for concrete, sand, soil and other construction materials boosted mining and quarrying activities. Similarly, manufacturing activities got a boost from improved political situation (no strikes and labor disruptions) and energy supply, thanks to the NEA’s excellent efforts in managing existing stock of energy and adding additional units to the grid (domestic as well as imported). Manufacturing, and electricity, gas and water subsectors are expected to contribute 0.6 and 0.3 percentage points, respectively, to the overall GDP growth. Furthermore, construction activities accelerated due to the pick up in post-earthquake reconstruction works and substantial improvement in works related to large infrastructure projects (Melamchi, Upper Tamakoshi, etc).

Fourth, the demand dampening from deceleration of remittances and marginal effects of demonetization were dominated by the surge in demand following the normalization of supplies and increasing tourist arrivals, thus ensuring a robust services growth. Wholesale and retail activities, which were severely crippled by supplies disruption and grew at a negative 2.5% in FY2016, are projected to grow by 9.8% (thus contribution 1.3 percentage points to the overall GDP growth). Similarly, there were improvements in tourism activities (contributed by domestic tourism as well as international tourists arrivals), transportation and communication (no notable strikes and blockade), and real estate business. Election related expenses will also give boost to services activities.

Hence, a large base effect together with favorable exogenous factors (good monsoon rains and remittances-backed demand of imported as well as domestically produced goods, whose supplies gradually normalized) and to some extent the government’s efforts led to this impressive growth rate. An important challenge would be to sustain this rate. It is easy to move from almost nil growth to over 6% growth. But, it is difficult to sustain it at this level. It requires a rapid and meaningful structural transformation. The CBS will likely revise down this projection in April 2018, when it releases the revised estimate. The reason is that the services output growth looks a bit more optimistic.

On the expenditure side, private fixed investment seems to have increased to 26.5% of GDP from 21.7% of GDP in FY2016. Overall, fixed investment is expected to reach 33.8% of GDP. Consumption accounted for about 89.7% of GDP. Trade deficit is projected to widen to 32.3% of GDP from 29.9% of GDP in FY2016.

The economy can sustain growth of over 7% with an appropriate mix of macroeconomic strategies, financial arrangements, smart project execution, and supportive institutions and policies. Government has an important role to play in providing critical infrastructure, addressing market failures, designing a growth-enhancing tax regime, and implementing business-friendly policies to usher in a meaningful structural transformation. It also needs to enhance both the quantum and quality of public capital spending to over 8 percent of GDP annually. Given the sound fiscal space, though Nepal doesn’t have a shortage of funds until medium-term, a dearth of capacity to fully execute the budget and finish projects on time may prove problematic.

Achieving and sustaining a high growth rate is critical to achieve the long-term goal of becoming a prosperous middle-income country by 2030. Hence, implementing the vision of a rapid economic transformation would require consistent and committed political leadership, and a competent bureaucracy. This would form the institutional fabric that helps translate good economics into good politics with economic development as the core theme. It ensures shared prosperity, makes reversibility of policies costly, enhances individual’s and firm’s confidence in the economy, and encourages the bureaucracy to provide faster and better service delivery.